China’s economy is slowing in 2025 as deflationary pressures, weak property investment, sluggish retail sales, and contracting credit growth weigh on momentum. Despite reporting 5.3% growth in the first half of the year, fresh data highlights fading investment, subdued consumer demand, and a prolonged property slump. Policymakers face limited room for stimulus as structural challenges, demographic shifts, and global trade tensions deepen concerns about the sustainability of China’s growth trajectory.

China’s Economy Faces Mounting Pressures

China’s economy is facing a serious test in 2025, grappling with structural challenges, deflationary pressures, and global uncertainties. Despite reporting a GDP growth of 5.0 percent in 2024 and 5.3 percent in the first half of 2025, recent monthly data points to a fading momentum. Several key economic indicators including fixed-asset investment, property investment, retail sales, industrial production, and credit growth show signs of weakness, raising doubts about the sustainability of China’s recovery.

Policymakers are under growing pressure to introduce stronger stimulus measures, but deep-rooted problems such as a fragile property sector and weak consumer sentiment continue to act as roadblocks.

Fixed-Asset Investment Shows Weakest Growth in Years

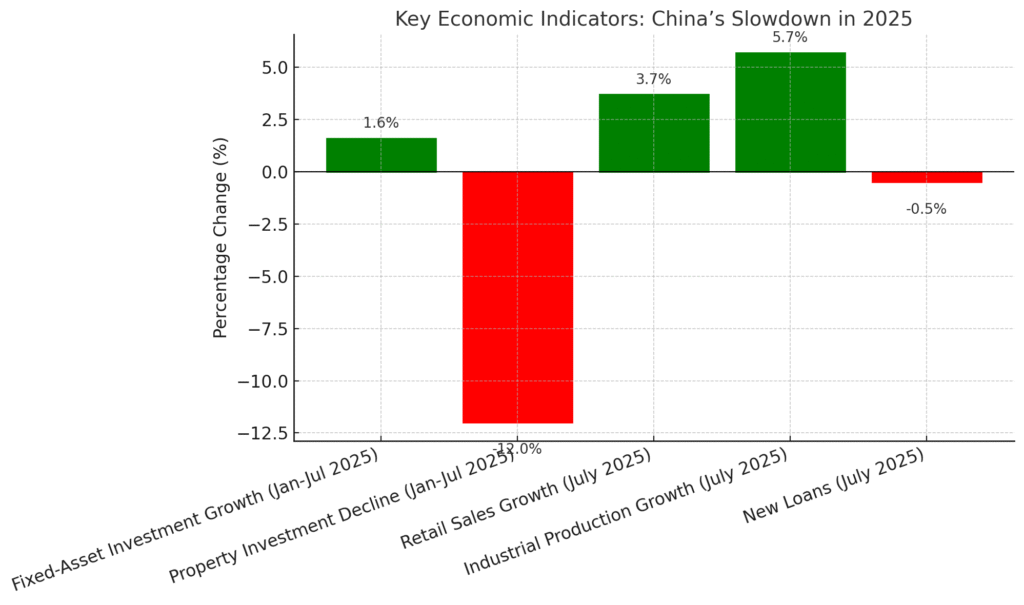

Fixed-asset investment grew by just 1.6 percent in the first seven months of 2025, the slowest pace in over five years. This was down from 2.8 percent growth recorded in the first half of the year. The decline reflects growing economic uncertainty and fiscal strain, with private investment dropping 1.5 percent during the period, marking its weakest performance since September 2020. Excluding real estate, fixed-asset investment performed better at 6.6 percent, suggesting resilience in high-tech and strategic manufacturing sectors.

However, the overall weakness indicates reduced capital expenditure by businesses and local governments, which could further weigh on economic activity, given that investment contributed around 1.3–1.5 percentage points to GDP growth in 2024.

Property Sector in Prolonged Decline

The property sector, once the backbone of China’s growth, continues to face deep stress. Property investment plunged 12 percent in the first seven months of 2025, compared to a 10.7 percent decline in the first five months. This is the steepest drop since the pandemic lows of 2020. New home prices fell 2.8 percent year-on-year in July, while new construction starts collapsed 23 percent through late 2024. Since most Chinese households hold their wealth in real estate, the downturn has already erased an estimated 18 trillion dollars in household wealth.

Analysts warn that the slump is likely to remain a drag on growth for 5–15 years in certain cities. Although Beijing has eased mortgage rates and removed some home purchase restrictions, such measures have not produced meaningful results. The real estate crisis alone is estimated to cut about three percentage points from GDP each year, considering both direct and indirect effects.

Retail Sales Falter as Consumer Confidence Stays Low

Retail sales, an important measure of consumer activity, rose only 3.7 percent in July 2025, down from 4.8 percent in June. This fell short of analysts’ expectations of 5.4 percent and reflects fragile consumer confidence. Declining property values, coupled with deflationary pressures, are discouraging households from spending. While consumer trade-in programs and appliance subsidies boosted consumption in late 2024, their impact has now diminished.

Household consumption growth is estimated at 3.5–4 percent, contributing 1.3–1.6 percentage points to GDP in 2024, but it remains insufficient to drive growth in 2025. The weakness is most visible in top-tier cities such as Beijing and Shanghai, where consumption growth is lagging behind the national average.

Industrial Production Slows After Strong First Half

Industrial production rose 5.7 percent in July 2025, compared to 6.8 percent in June. Though the slowdown is partly due to extreme weather disruptions and a high base effect, it marks the weakest expansion since November 2024. The manufacturing sector has been one of the few bright spots, with high-tech and export-driven industries posting strong gains earlier in the year.

For instance, transportation equipment and electronics recorded double-digit growth. Still, overcapacity in industries such as steel and solar is contributing to deflationary pressures and rising trade tensions with other countries. Analysts caution that if external demand weakens further, industrial output could face sharper declines.

Credit Contraction Highlights Weak Private Sector Demand

Perhaps the most alarming signal came in July 2025, when yuan-denominated new loans contracted for the first time in 20 years. Total Social Financing growth slowed to a record low of 7.8 percent year-on-year, while bank asset growth excluding government bonds dropped below 6 percent. The People’s Bank of China had earlier cut rates to 1.4 percent and injected one trillion yuan in liquidity, but the measures failed to boost lending.

Weak borrowing by private firms and local government financing vehicles underscores fragile confidence. Analysts point out that banks are still reluctant to lend to private companies, preferring state-owned enterprises instead, which may deepen investment and consumption slowdowns.

Deflationary Pressures and Export Dependence

China has been battling deflation for two years, with the GDP deflator projected at -0.2 percent in 2025. Producer prices fell 3.6 percent year-on-year in July, while consumer inflation hovered near zero. This environment encourages households to postpone purchases, further suppressing demand. On the external front, exports remain a vital growth driver, rising 7.2 percent in July and accounting for over 31 percent of GDP growth in the first half of 2025.

However, dependence on exports makes China vulnerable to trade tensions, particularly with the United States. Tariffs of up to 145 percent were imposed earlier in 2025 before a temporary truce, but risks remain high.

Policy Challenges and Limited Options

China’s government is considering more aggressive fiscal measures, including raising the budget deficit to 4 percent of GDP and issuing 3 trillion yuan in special bonds to fund infrastructure and consumer subsidies. While monetary easing continues, it is constrained by the risk of yuan depreciation and potential capital outflows.

Beijing is also exploring childcare subsidies to reduce household burdens and expanding trade-in programs to include services. Property stabilization efforts include financing for “whitelisted” projects and converting unsold commercial real estate into affordable housing, but funding constraints limit progress.

Long-Term Structural Problems

China’s traditional investment-led growth model is showing signs of exhaustion, with diminishing returns on infrastructure and credit-heavy policies. High savings rates drive investment, but weak household consumption due to limited welfare support prevents meaningful rebalancing. Meanwhile, demographic issues like a shrinking working-age population and declining fertility rates pose long-term threats to sustainable growth.

Outlook and Global Implications

Analysts forecast China’s GDP growth at 4.6 percent in 2025, below the official target of 5 percent, and expect a further slowdown to 4.2 percent in 2026. While near-term stimulus could provide temporary relief, structural reforms are necessary to address imbalances and unlock consumer demand. China’s slowdown has global repercussions, given its role as the world’s largest exporter and accounting for 18 percent of global GDP.

A weaker China could dampen commodity demand, disrupt supply chains, and heighten financial volatility worldwide. At the same time, Beijing’s push for self-reliance in advanced sectors such as semiconductors, AI, and green technology could intensify strategic competition with the United States and other economies.

A Critical Perspective

Despite Beijing’s claims of hitting growth targets, skepticism remains over the accuracy of official data. Alternative indicators such as declining cement output, weaker diesel demand, and lower asphalt plant utilization suggest slower real activity. Critics argue that reliance on state-led investment and export dependency, without deeper reforms, risks masking vulnerabilities and leaving the economy exposed to further shocks.

In conclusion, while China has tools at its disposal to cushion the slowdown, the road ahead is complicated. The combination of structural challenges, deflationary risks, and geopolitical uncertainties means the world’s second-largest economy is entering a phase of prolonged adjustment that will test policymakers’ ability to balance stability with reform.