Global markets are betting on a September Federal Reserve rate cut after Chair Jerome Powell’s much-anticipated Jackson Hole speech signaled a policy pivot. Jefferies’ Chief Market Strategist David Cerbos, also mentioned as a possible future Fed chair, welcomed the shift but criticized the Fed for acting too late and keeping monetary policy unnecessarily restrictive. Despite record stock market highs, tight credit spreads, and steady economic growth, Cerbos argues that interest rates remain higher than needed, preventing the economy from reaching its full potential.

Jefferies Says ‘No reason’ for Fed to be waiting this long for rate cuts

Global financial markets are once again betting heavily on a September rate cut following Federal Reserve Chair Jerome Powell’s much-discussed pivot at Jackson Hole on Friday. The remarks have fueled optimism among investors and policymakers who see a shift in the Fed’s stance on inflation, tariffs, and employment.

To discuss the developments, Jefferies’ Chief Market Strategist David Cerbos, who is also mentioned as a potential candidate for the next Fed chair, weighed in on the implications of Powell’s speech and the broader economic environment.

Cerbos welcomed the pivot, stating that the Fed had been “stubborn” in its views on inflation, tariffs, and employment. He acknowledged that Powell’s recalibration of long-term goals was encouraging but noted the move was “a little late.” According to him, there was no reason other than political motivations for delaying a sequence of rate cuts that could have come earlier.

When asked about the impact of tariffs and the uncertainties surrounding them, Cerbos argued that the Fed overreacted to the political spectacle at the White House earlier this year, when President Trump announced aggressive tariff figures. He emphasized that the president’s approach was more of a tactical negotiation strategy rather than a structural economic threat.

“People got to the table fast when they saw those numbers,” Cerbos explained, adding that the market understood the strategy much earlier than the Federal Open Market Committee. He noted that by May and June, markets had already begun recovering sharply, even though the Fed was not providing the support it could have.

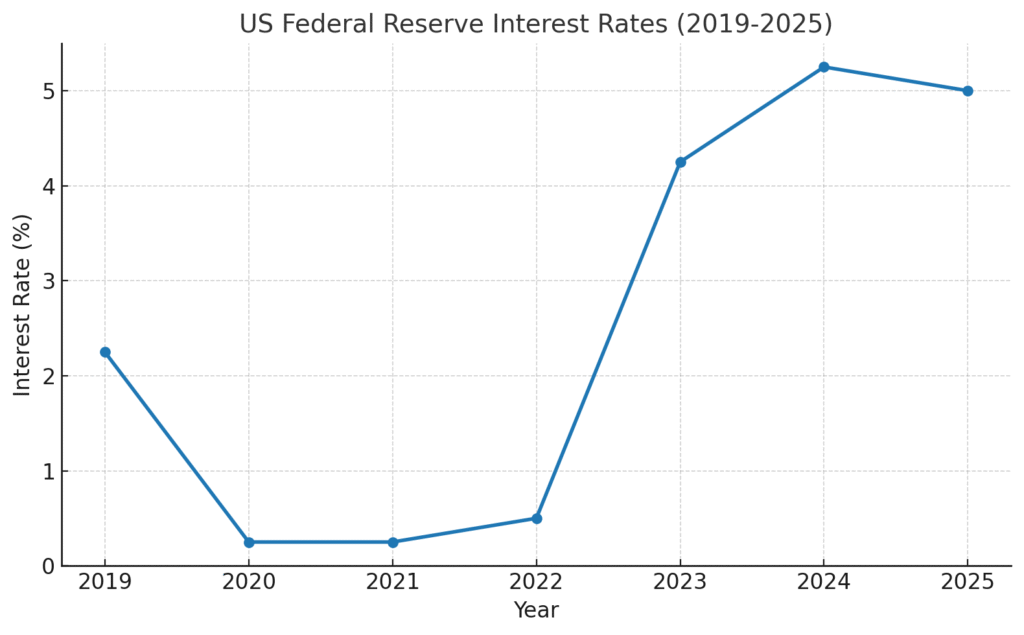

Despite stocks at record highs, tight credit spreads, and an economy performing well by most measures, Cerbos criticized the Fed for maintaining restrictive monetary policy. He argued that inflationary risks from tariffs were overstated, and that current interest rates remain unnecessarily high.

Drawing comparisons with pre-COVID conditions, Cerbos highlighted that rates were around 2% when the Fed’s balance sheet was about 20% of GDP. He suggested that the U.S. could sustain much lower interest rates without overheating the economy. According to him, restrictive monetary policy is now standing in the way of greater economic growth.

Cerbos also pointed to the ongoing transition away from what he described as the excesses of the previous administration. He highlighted the shift toward “Reprivatization,” where jobs and functions are moving from the public sector back into the private sector. While this transition may create temporary jitters in the labor market, he believes the economy would be better served by a more accommodative policy stance rather than restrictive measures.

“There’s no reason to tie one hand behind our back,” Cerbos argued. “Things are good, but they could be better. We could have unemployment closer to 3.25% or 3.5% if policy were more supportive.”

Looking ahead, Cerbos expects the U.S. economy to gain further strength as reprivatization accelerates into late 2025 and 2026. He remains confident that the Fed’s pivot, coupled with easing financial conditions, can create a stronger foundation for growth. However, he warned that unnecessary monetary tightening could complicate the recovery and dampen the momentum that markets and businesses have already started to build.

As investors price in the likelihood of a September rate cut, the debate continues on whether the Fed’s shift is timely enough to support economic expansion without introducing new risks. For now, optimism in financial markets suggests that Powell’s Jackson Hole pivot has already reshaped expectations for the months ahead.

Disclaimer:

The information provided in this article is for informational and educational purposes only. It should not be considered as financial, investment, or trading advice. Market conditions are subject to rapid change, and readers are advised to conduct their own research or consult with a qualified financial advisor before making any investment decisions. The views expressed by market strategists or analysts mentioned are their own and do not necessarily reflect the views of this platform.