Eurostat data shows the euro area household saving rate rose to 15.4% in Q2 2025, while the business profit share declined to 39.1%. Household investment stayed stable at 9%, and corporate investment weakened due to lower capital formation.

Euro Area Household Saving Rate Climbs to 15.4% in Q2 2025

The latest seasonally adjusted quarterly European sector accounts released by Eurostat, the statistical office of the European Union, reveal that the household saving rate in the euro area increased to 15.4% in the second quarter of 2025, up slightly from 15.2% in the first quarter of the year. This improvement in the saving rate reflects a broader economic trend of moderate income growth outpacing consumption, signaling that households are maintaining cautious optimism amid an evolving macroeconomic environment.

The data show that household gross disposable income rose by 1.0% quarter-over-quarter, while individual consumption expenditure increased by 0.7%. The slower growth in consumption compared with income explains the uptick in savings. In other words, households earned more but spent proportionally less, choosing to set aside a higher portion of their income.

At the same time, the household investment rate in the euro area remained steady at 9.0% in Q2 2025, mirroring the growth rate of gross fixed capital formation and gross disposable income. Both metrics increased by 1.0% during the quarter. This indicates that while households are saving more, their investment behavior remains consistent, with stable patterns of capital allocation towards residential and other long-term assets.

Looking at the broader trend over the past two years, the household saving rate has shown gradual growth. It stood at 14.2% in the third quarter of 2023, rising to 14.8% in Q4 2023, then reaching 15.2% in the first quarter of 2024 and 15.4% in the second quarter of 2024. Although there were minor quarterly fluctuations, the overall trajectory suggests that European households have been steadily rebuilding their financial buffers. The investment rate has hovered between 9.0% and 9.7% since 2023, indicating relative stability despite changing economic conditions.

In terms of gross disposable income, households recorded a quarter-over-quarter growth of 0.9% in Q1 2025, followed by 1.0% in Q2 2025. This consistent income growth, combined with restrained consumption, underscores the resilience of household finances in the euro area.

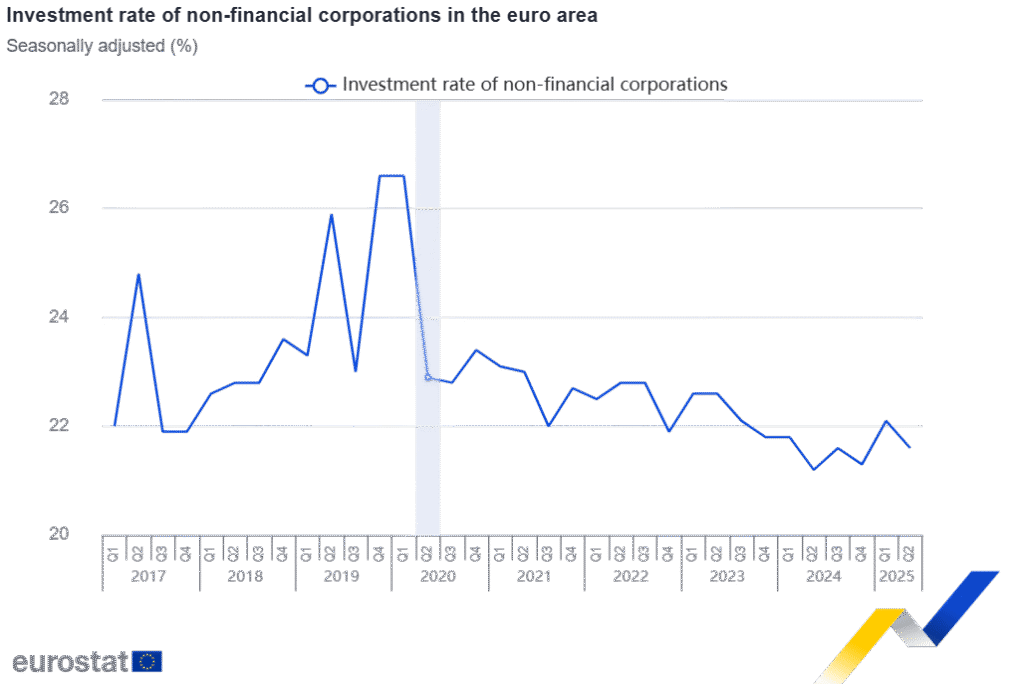

However, not all sectors displayed similar strength. The non-financial corporate sector reported a decline in profitability and investment during the same period. The profit share of euro area businesses decreased from 39.3% in the first quarter of 2025 to 39.1% in the second quarter.

This decline was largely due to a faster increase in business compensation of employees (including wages and employers’ social contributions) and taxes less subsidies on production, which grew by 1.1%. Meanwhile, gross value added—a key measure of corporate output—rose by 0.9%, indicating that production gains were not enough to offset rising costs.

The business investment rate also declined, falling from 22.1% in Q1 2025 to 21.6% in Q2 2025. This decrease was linked to a 1.4% drop in gross fixed capital formation, even though gross value added increased by 0.9%. The data suggest that while business output continued to expand, investment activity slowed, possibly reflecting cost pressures, higher borrowing costs, or a cautious outlook on future demand.

Over the longer term, the profit share of non-financial corporations has gradually declined from 41.1% in Q3 2023 to 39.1% in Q2 2025. Similarly, the corporate investment rate has fluctuated within the 21–22% range, showing some cyclical dips but maintaining overall stability.

In historical context, Eurostat noted that significant peaks in business investment were recorded in Q2 2017, Q2 2019, Q4 2019, and Q1 2020. These spikes were mainly due to large imports of intellectual property products, which reflected the effects of globalization and multinational corporate restructuring across the European economy.

The euro area’s current sectoral dynamics highlight a clear contrast between households and businesses. While households continue to strengthen their savings and maintain stable investment rates, corporations face narrowing profit margins and softer capital spending. The rise in employee compensation, while positive for household income, is contributing to pressure on corporate profitability.

Overall, the data from the second quarter of 2025 paint a mixed picture of the euro area economy. Households are in a stronger financial position, with increasing savings and steady income growth, while non-financial corporations are navigating cost pressures and reduced investment appetite. The European economy thus finds itself in a delicate balance—supported by resilient households but weighed down by slowing business investment.

The coming quarters will be crucial in determining whether this cautious optimism among consumers can translate into renewed momentum for corporate growth and broader economic expansion.