Chinese net new loans fell by ~50 billion Yuan in July:China has reported its first contraction in net new bank loans since 2005, with borrowings shrinking by nearly 50 billion yuan in July. The drop, driven by households and companies repaying debt instead of taking new loans, signals weakening economic momentum. Compared to an expansion of around 5 trillion yuan at the start of the year, this sharp reversal highlights growing caution in China’s economy amid slowing demand and persistent financial pressures.

Chinese net new loans fell by ~50 billion Yuan in July

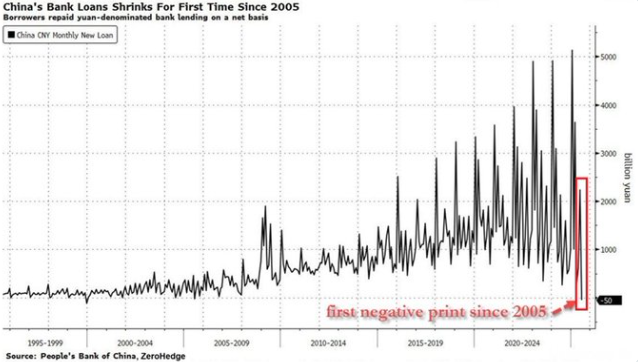

Chinese net new loans fell by ~50 billion Yuan :In a development that has raised concerns about the health of the world’s second-largest economy, China has reported its first decline in net new bank loans since 2005. According to data from the People’s Bank of China, net new yuan-denominated loans fell by approximately 50 billion yuan in July, a sharp reversal from the expansionary trend that has defined Chinese lending for nearly two decades.

Chinese net new loans fell by ~50 billion Yuan :This contraction is particularly striking when contrasted with the surge earlier this year. At the start of 2025, Chinese banks had extended nearly 5 trillion yuan in net new loans, underscoring the robust role of credit growth in sustaining China’s economic engine. Yet, by mid-year, that momentum has not only slowed but shifted into negative territory—a clear sign that borrowers are repaying loans on a net basis rather than taking on new debt.

Chinese net new loans fell by ~50 billion Yuan :The decline is not simply a technical fluctuation. It reflects deeper structural challenges within the Chinese economy. For decades, China’s growth has been fueled by heavy borrowing, both by households seeking property investments and by corporations expanding production capacity. The sharp contraction in July suggests that both households and companies are now becoming more cautious, hesitant to increase their leverage in an environment of economic uncertainty.

Chinese net new loans fell by ~50 billion Yuan :Household sentiment in particular appears to have weakened. For years, Chinese families were major drivers of loan growth, especially through mortgages tied to the property sector. However, the prolonged real estate downturn, coupled with falling home prices and defaults among major developers, has eroded confidence. Many households are now more inclined to pay down existing debts rather than take on new ones, a behavior that directly contributes to the negative loan figures.

Chinese net new loans fell by ~50 billion Yuan :On the corporate side, businesses face mounting pressures from slower domestic demand, weaker exports, and global economic headwinds. Rather than expanding with borrowed funds, companies are cutting back, consolidating, and in some cases repaying existing loans. This trend indicates that investment appetite is declining—a troubling signal for policymakers who rely on corporate borrowing as a driver of growth and job creation.

Chinese net new loans fell by ~50 billion Yuan :The decline in new loans is especially concerning given the central role of credit in China’s growth model. For years, policymakers in Beijing have relied on credit expansion as a tool to stimulate activity during periods of slowdown. Each time the economy showed signs of weakness, banks would ramp up lending, supporting infrastructure spending, property development, and consumer borrowing. The fact that borrowers themselves are now pulling back, even as lending capacity exists, shows that confidence is weakening at a fundamental level.

Chinese net new loans fell by ~50 billion Yuan :From a macroeconomic perspective, the contraction highlights the fragility of China’s current recovery. After emerging from pandemic-related disruptions, the economy initially appeared to regain strength, with a burst of lending at the beginning of the year. However, the subsequent reversal demonstrates that this momentum may not be sustainable without stronger underlying demand. With consumer spending subdued and private sector investment lagging, credit growth is no longer translating into the same levels of economic activity as in the past.

Chinese net new loans fell by ~50 billion Yuan :The timing also underscores broader challenges facing Chinese policymakers. The government has been attempting to balance the need for stimulus with concerns about long-term financial stability. Excessive reliance on debt has already created risks in the property sector and among heavily leveraged local governments. Now, with borrowers reluctant to take on more credit, traditional stimulus levers may be less effective.

Chinese net new loans fell by ~50 billion Yuan :Global investors are closely watching these developments. A slowdown in Chinese lending not only signals domestic weakness but also has international implications. China is a major driver of global demand, and reduced economic momentum could affect commodity markets, global trade, and the financial outlook for countries heavily linked to Chinese growth.

The July data could be an early warning sign of deeper economic headwinds ahead. If households and corporations continue to repay debt on a net basis, it will be difficult for China to maintain the high levels of growth it has enjoyed for decades. The challenge for policymakers is now twofold: to restore confidence among borrowers while also ensuring that lending does not fuel unsustainable bubbles.

For now, the negative print serves as a stark reminder that China’s growth model is under strain. The fact that new loans have turned negative for the first time since 2005 marks not just a statistical anomaly but a signal of shifting behavior among borrowers. Unless confidence is restored, credit growth could remain weak, limiting the ability of stimulus measures to reignite the economy.

China’s long-standing reliance on credit expansion to fuel growth has entered a new and uncertain phase. Whether this contraction proves to be a temporary blip or the beginning of a more prolonged period of deleveraging will depend on how households, corporations, and policymakers respond in the months ahead. What is clear, however, is that the July loan data marks an important turning point, highlighting the risks of an economy slowing under the weight of its own debt-driven past.

Disclaimer:

The information presented in this article is based on publicly available data and reports. It is intended for informational and educational purposes only and should not be considered as financial or investment advice. Readers are encouraged to conduct their own research or consult with a qualified professional before making any financial decisions.